Benefits for people, by people

At Chard Snyder, we do more than administer benefits and compliance services. We provide partnership with a higher purpose—simplifying life for employers, and helping participants make the most of their benefits and save for healthcare needs.

Our expert team is supported by advanced technology that ensures ease and efficiency. The result is a simple, smooth experience employers and plan participants can count on. That's our promise as we aspire to make a difference for others, every day.

-

Savings and Spending Accounts

These are pre-tax accounts designed to help you save money for the services you already pay for like healthcare, dependent care and parking. We offer: Flexible Spending Accounts (FSA), Health Reimbursement Arrangements (HRA), Health Savings Accounts (HSA), Lifestyle Spending Accounts (LSA), and Commuter Benefits.

-

Benefit Continuation Services

We provide services and plans that reach beyond the walls of employment to ensure that not only current employees are taken care of, but employees who have moved on or retired are eligible for benefits like COBRA and Billing Administration services.

-

Plan Document Services

Get the comfort of knowing your plan documents are created, revised and maintained to assure you’re in compliance at all times. Our team stays current on relevant industry changes and utilizes the latest document management tools to let us proactively communicate with you and deliver on time.

-

FMLA Leave Administration

FMLA Leave (Family and Medical Leave Act) is gaining attention as more employees utilize the law, making it more important than ever to have a fully dedicated group to ensure the process is managed properly. With the help of our compliance-focused team, we make the process seamless and worry-free.

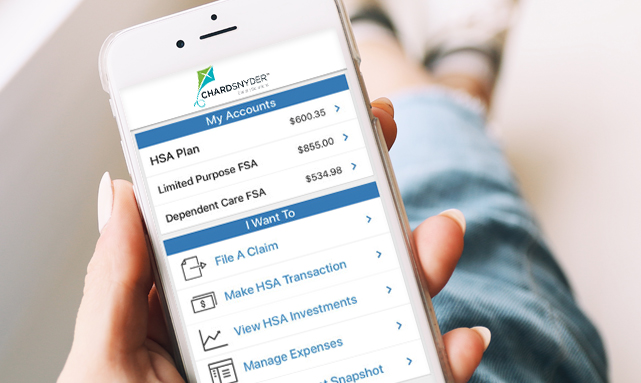

Mobile App

The Chard Snyder Mobile App provides a simple, easy way to manage your Chard Snyder savings and spending accounts from anywhere. Designed for convenient on-the-go access, our mobile app lets you securely view account balances, submit claims, send payments, manage expenses, and even scan items for eligibility with the touch of a finger.

- Employees

- Employers & Advisors

We know navigating the world of employee benefit plans can be overwhelming and you likely have questions. We’ve simplified the process and our tools to help make it easier for you. You can find answers in our Support Center or if you’d rather talk to a person, give us a call.

We provide expert benefits administration services for clients nationwide, from small businesses to large employers across a wide variety of industries. We offer one-stop shopping for the most popular employee benefits to save you time, meet your unique needs, and make things easy and convenient for plan participants.

Everyone on the Chard Snyder team is responsive, kind, and very helpful to our staff and former employees/retirees. They are great at helping me understand things, provide great customer service, and are easy to work with. Our support person for COBRA and retiree billing is outstanding.